It's finally happening: A schism between Greece and the European establishment has rattled investors, filling them with a sense of dread they haven't felt in years.

The Greek debt drama, which first started in early 2010, is coming to a head now as Greek Prime Minister Alexis Tsipras has called for a popular referendum on the latest bailout proposal from the European establishment and the International Monetary Fund, throwing the country's position within the Eurozone into jeopardy. Global markets were shaken by the weekend twists, with the Euro Stoxx 50 index falling 4.2 percent.

After the referendum was announced, lines quickly formed outside Greek ATMs. The deal to be voted on has been retracted by the institutions, making this essentially a vote on whether the Greek people want to stay in the euro or restore the drachma — a vote the European establishment pushed back against when it was first proposed in 2011.

Related: ‘Grexit’ Chances Increase with Greek Referendum

The pressure is building: On Sunday, the European Central Bank decided to put a freeze on its liquidity support for Greek banks. Athens was in turn forced to impose capital controls and enact a bank holiday as the country prepares for the vote on July 5. Greece's current bailout program ends on June 30, the same date it owes the IMF a $1.8 billion debt payment.

The tranquility investors have grown accustomed to — comfortable in the belief that any negative catalyst would be papered over with more cheap money stimulus — has been shattered as bourses in Asia and Europe plunged in Monday morning trading.

Since the Federal Reserve unleashed its QE3 bond buying program in 2012, the Bank of Japan launched "Abenomics," the European Central Bank finally initiated its bond buying stimulus and the People's Bank of China began to actively support a stock market bubble, global financial markets acted as if nothing would ever bother them again. The S&P 500's run of not succumbing to a typical 10 percent correction is already at the third-longest in history, exceeded only by the last two bull markets.

Whereas the last two iterations of the "it's different this time" madness were driven by dot-com fever and the belief that home prices would never fall, now it's all about a fervent belief in central banks: When central bankers are pumping out cheap money, financial assets can only ever rise. "Don't fight the Fed" and all that.

The Achilles' heel, the point of vulnerability, in this thinking has been revealed by the Syriza hard leftists in Athens: Debts can be dismissed, even if they are owned by central banks and the IMF.

Related: Why the Greek Crisis Could Mean Cheaper Oil

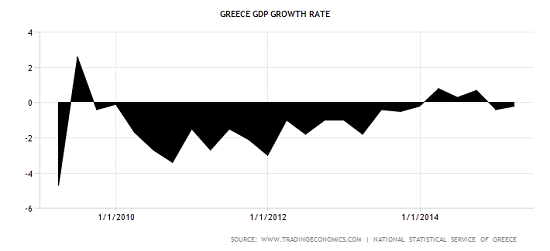

In their words, social justice and national pride are more important than preserving a flawed currency union, protecting German taxpayers exposed to a Greek default or resisting an Iceland-style bank nationalization and recapitalization. Tsipras and his party were elected earlier this year by a desperate people suffering punishing budget austerity, a 50 percent youth unemployment rate and an economy tipping back into recession. They are the third government to come to power since the crisis began.

And they are in open revolt against the debt servitude central bank largesse depends on. A report on its public debt by the Hellenic Parliament clamors for default, dismissing its debt as "illegal, illegitimate, and odious."

Michala Marcussen, global head of economics at Societe Generale, breaks down what to expect next:

If the Greeks vote to accept bailout terms, Tsipras would likely be forced to resign and call new elections. Current polling shows he would hold his parliamentary majority in a new election, revealing the try-to-have-it-all preferences of the Greek people right now. They want less austerity but to remain within the euro — something that probably isn't possible.

Under this scenario, Greece would likely default not just on the June 30 IMF payment but a payment to the ECB due on July 20.

Related: Why It’s Time for Greece to Call the Euro Quits

If the referendum rejects the bailout terms, this would mark the first step towards a “Grexit,” or Greek exit from the euro, as European officials have shown no indication of being willing or politically able to offer Greece a better bailout deal. Polling shows a majority of German people want Greece kicked out of the euro, for instance, with only 40 percent believing it should stay.

Greece's president has previously threatened to resign should Grexit occur — which, because of the machinations of voting laws, could result in a general election and a political crisis.

Global financial contagion is a concern through a variety of possible mechanisms, including the risk that Syriza’s example will encourage anti-euro politics in Spain and Italy, bank losses on debt write-offs and payouts connected to the triggering of credit default swaps.

Evidence that the Greece situation is undercutting central bank omnipotence comes out of China, where the Shanghai Composite fell into bear market territory, down more than 20 percent from its high, despite a double dose of policy easing from the PBoC over the weekend. The real test will come should the global selloff encourage Fed officials to tease a fourth round of bond buying stimulus — backing off of their teases of a rate hike later this year.

If stocks don't rebound in response, as they did in October when St. Louis Fed President James Bullard hinted at QE4 in the midst of Ebola-driven market turmoil, things could get ugly in a hurry.

Top Reads from The Fiscal Times:

- Why Vladimir Putin Wants Texas to Secede from the U.S.

- The Pope’s Manifesto Could Destroy the U.S. Economy

- Slideshow: 16 Companies Taking Some ‘Junk’ Out of Their Food