Don’t Feel Like a Chump When You Close on Your New Mortgage

Mortgage closing costs dropped 7 percent over the past year, falling to $1,847 on a $200,000 loan, according to a new analysis by Bankrate.

Typical closing costs varied by state, ranging from $2,163 in Hawaii to $1,613 in Ohio. You can find the average rate for your state in the table below.

Lenders compete for business, so shopping around with at least three mortgage providers can help you reduce the fees associated with your loan. “Homebuyers have more say over closing costs than they think,” Bankrate Senior Mortgage Analyst Holden Lewis said in a statement.

Even as banks lower their mortgage fees, they’re increasing fees in most other categories, according to MoneyRates.com.

While lower mortgage fees are good news for homebuyers and those refinancing their loans, the average saving amount to just $140. That’s not much relative to the total costs associated with buying a house. The average down payment for homebuyers in the first quarter of 2015 was $57,710, for example.

Related: Want Your Own Home? Here’s How to Do the Math

The costs don’t stop once the buyers move in. On top of mortgage payments, homeowners face an average of more than $6,000 in additional costs related to their house, including homeowners insurance, property taxes and utilities.

The National Association of Realtors expects home prices to increase 6.5 percent this year to a median $221,900, which would put them at the same level as their 2006 record high.

For buyers, better news than the lower mortgage fees is that rates remain relatively low, falling to 3.98 percent last week, per Freddie Mac.

Closing costs | |||

|---|---|---|---|

| State | Average origination fees | Average third-party fees | Average origination plus third-party fees |

| Alabama | $1,066 | $776 | $1,842 |

| Alaska | $935 | $922 | $1,857 |

| Arizona | $1,208 | $761 | $1,969 |

| Arkansas | $1,057 | $760 | $1,817 |

| California | $937 | $896 | $1,834 |

| Colorado | $1,192 | $719 | $1,910 |

| Connecticut | $1,074 | $960 | $2,033 |

| Delaware | $904 | $924 | $1,828 |

| District of Columbia | $1,077 | $718 | $1,794 |

| Florida | $1,028 | $778 | $1,806 |

| Georgia | $1,058 | $821 | $1,879 |

| Hawaii | $1,033 | $1,130 | $2,163 |

| Idaho | $894 | $788 | $1,682 |

| Illinois | $1,080 | $767 | $1,847 |

| Indiana | $1,067 | $770 | $1,837 |

| Iowa | $1,161 | $762 | $1,923 |

| Kansas | $1,047 | $753 | $1,800 |

| Kentucky | $1,060 | $737 | $1,797 |

| Louisiana | $1,060 | $817 | $1,877 |

| Maine | $897 | $830 | $1,727 |

| Maryland | $1,093 | $742 | $1,835 |

| Massachusetts | $905 | $851 | $1,756 |

| Michigan | $1,072 | $746 | $1,818 |

| Minnesota | $1,067 | $689 | $1,757 |

| Mississippi | $1,046 | $837 | $1,884 |

| Missouri | $1,040 | $792 | $1,833 |

| Montana | $1,062 | $855 | $1,917 |

| Nebraska | $1,047 | $770 | $1,817 |

| Nevada | $1,002 | $848 | $1,850 |

| New Hampshire | $1,084 | $750 | $1,835 |

| New Jersey | $1,181 | $913 | $2,094 |

| New Mexico | $1,076 | $876 | $1,952 |

| New York | $1,032 | $879 | $1,911 |

| North Carolina | $1,036 | $875 | $1,911 |

| North Dakota | $1,045 | $791 | $1,836 |

| Ohio | $933 | $681 | $1,613 |

| Oklahoma | $1,027 | $734 | $1,761 |

| Oregon | $1,080 | $785 | $1,864 |

| Pennsylvania | $1,055 | $678 | $1,733 |

| Rhode Island | $1,093 | $802 | $1,896 |

| South Carolina | $1,058 | $837 | $1,895 |

| South Dakota | $1,055 | $704 | $1,759 |

| Tennessee | $1,033 | $773 | $1,806 |

| Texas | $1,031 | $833 | $1,864 |

| Utah | $909 | $788 | $1,697 |

| Vermont | $1,074 | $862 | $1,936 |

| Virginia | $1,050 | $787 | $1,837 |

| Washington | $1,077 | $824 | $1,901 |

| West Virginia | $1,067 | $904 | $1,971 |

| Wisconsin | $1,047 | $723 | $1,770 |

| Wyoming | $874 | $814 | $1,689 |

| Average | $1,041 | $807 | $1,847 |

Bankrate.com surveyed up to 10 lenders in each state in June 2015 and obtained online Good Faith Estimates for a $200,000 mortgage to buy a single-family home with a 20 percent down payment in a prominent city. Costs include fees charged by lenders, as well as third-party fees for services such as appraisals and credit reports. The survey excludes title insurance, title search, taxes, property insurance, association fees, interest and other prepaid items.

Top Reads from The Fiscal Times:

- You’re Richer Than You Think. Really.

- The 10 Fastest-Growing Jobs Right Now

- The 5 Worst Cities to Raise a Family

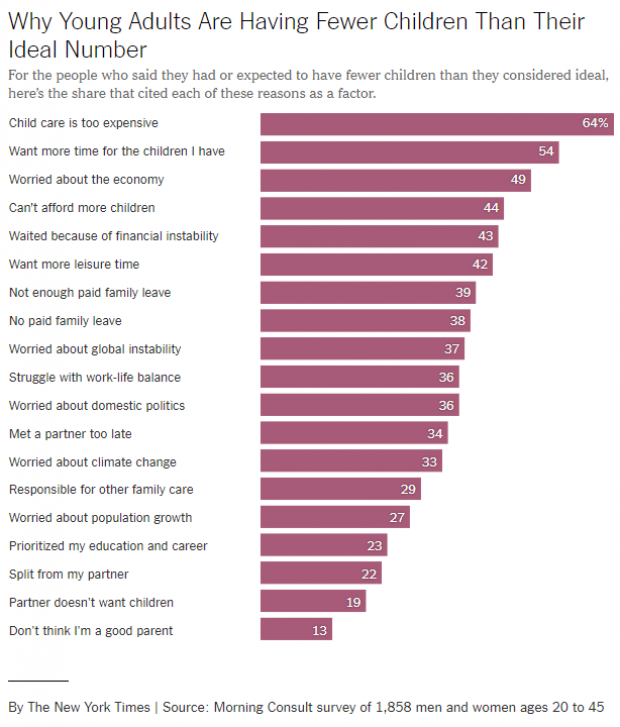

Chart of the Day: Why US Fertility Rates Are Falling

Babysit")

U.S. fertility rates have fallen to record lows for two straight years. “Because the fertility rate subtly shapes many major issues of the day — including immigration, education, housing, the labor supply, the social safety net and support for working families — there’s a lot of concern about why today’s young adults aren’t having as many children,” Claire Cain Miller explains at The New York Times’ Upshot. “So we asked them.”

Here are some results of the Times’ survey, conducted with Morning Consult. Read the full Times story for more details.

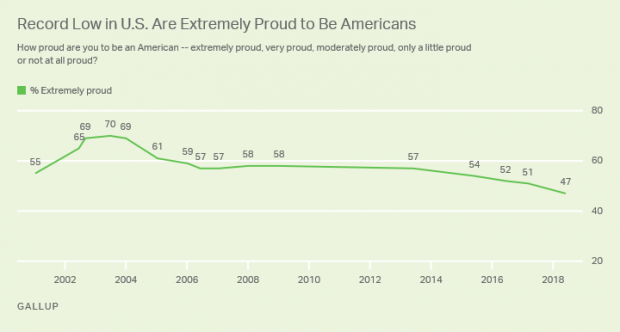

A Record Low 47% of US Adults Say They're 'Extremely Proud' to Be American

Gallup says that, for the first time in the 18 years it’s been asking U.S. adults how proud they are to be Americans, fewer than half say they are "extremely proud." Just 47 percent now say they’re extremely proud, down from 70 percent in 2003.

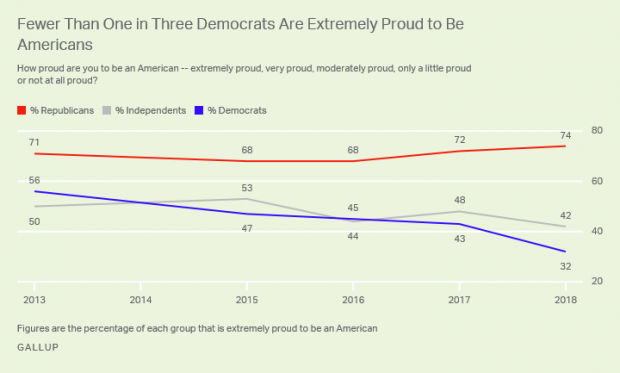

Another 25 percent say they’re “very proud” — but the combined 72 percent who say they’re extremely or very proud is also the lowest Gallup has recorded. Pride levels among liberals and Democrats have plunged since 2017. Overall, 74 percent of Republicans and just 32 percent of Democrats call themselves “extremely proud” to be American.

Pfizer Has Raised Prices on 100 of Its Products

Weeks after President Trump said that drugmakers were about to implement “voluntary massive drops in prices” — reductions that have yet to materialize — Pfizer has raised prices on 100 of its products, The Financial Times’s David Crow reports:

“The increases were effective as of July 1 and in most cases were more than 9 per cent — well above the rate of inflation in the US, which is running at about 2 per cent. … Pfizer, the largest standalone drugmaker in the US, did decrease the prices of five products by between 16 per cent and 44 per cent, according to the figures.”

Crow notes that Pfizer also raised prices on many of its medicines in January, meaning that some prices have been hiked by nearly 20 percent this year. The drugmaker said that it was only changing prices on 10 percent of its medicines and that list prices did not reflect what most patients or insurers actually paid. The net price increase after rebates and discounts was expected to be in the “low single digits,” the company told the FT.

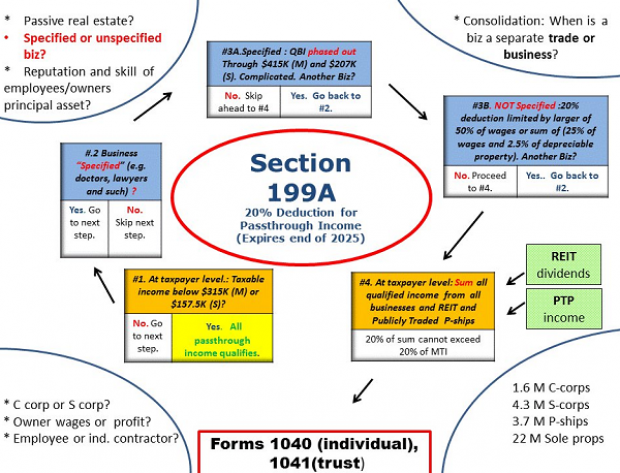

Chart of the Day: Pass-Through Tax Deductions Made Easy

The Republican tax overhaul was supposed to simplify the tax code, but most experts say it fell well short of the goal. Martin Sullivan, chief economist at Tax Analysts, tweeted out a chart of the analysis required to determine whether income qualifies for the passthrough tax deduction of 20 percent, and as you’ll see, it’s anything but simple.

A Conservative Bashes GOP Dysfunction on Spending Cuts

Brian Riedl, a senior fellow at the conservative Manhattan Institute, offers a blistering critique of congressional Republican’s problems cutting spending:

Since the Republicans took the House in 2011, nearly every annual budget blueprint has promised to balance the budget within a decade with anywhere from $5 trillion to $8 trillion in spending cuts. And yet, you may have noticed, the budget has not moved towards balance. This is because the budget merely sets a broad fiscal goal. To actually cut spending, Congress must follow up with specific legislation to reform Medicare, Medicaid, and all the other targeted programs. In reality, most lawmakers who pass these budgets have no intention whatsoever of cutting this spending. As soon as the budget is passed, the targets are forgotten. The spending-cut legislation is never even drafted, much less voted on.

The annual budget exercise is thus a cynical exercise in symbolism. Congress calculates how much spending must be cut over ten years to balance the budget. Then they pass legislation setting a goal of cutting that amount. Then they move on to other business. It’s like a baseball team announcing that they voted to win the next World Series, and then not showing up to play the season.

Read the full piece at National Review.