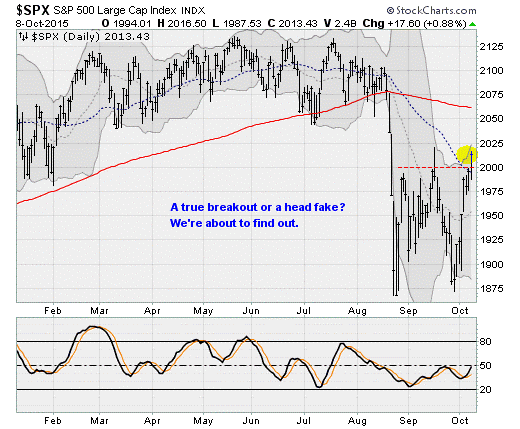

The past week has unleashed a fresh stock market uptrend for the first time in months, as large-cap stocks have rallied in seven of the last eight sessions and the Dow Jones Industrial Average has climbed back above 17,000.

The rebound is no surprise, given soft September payroll data and continued vulnerability in China — there is simply less and less justification for the Federal Reserve to raise rates this year. The stimulus junkies on Wall Street just got an early Christmas present. Even as the latest Fed meeting minutes, released Thursday, indicate that most of the bank’s policymakers continue to believe a rate hike will happen by the end of the year, future market odds keep dropping as inflation remains soft. The market doesn’t see a better-than-even chance of a hike until March 2016.

Related: Not So Fast, Janet — Why the September Jobs Report Really Matters

Technical indicators suggest this is just the start of a multi-month rally — likely lifting stocks through the end of the year in a typical "Santa Claus" rally before rate hike fears resurface.

For sure, there will be bumps along the way, such as the start of the third quarter earnings season.

After Thursday’s close, Alcoa (AA) kicked things off with disappointment: Earnings came in at just 7 cents per share vs. the 14 cents analysts were expecting. Revenues totaled $5.6 billion vs. the $5.67 billion expected. Adjusted operating profit margin fell to 12.5 percent vs. 16.6 percent last year. Shares dropped 4.6 percent in after-hours trading.

Overall S&P 500 earnings are expected to fall 5.1 percent for the quarter, which would mark the first back-to-back declines since 2009.

Related: U.S. Companies Are Dying Faster Than Ever

But as tradable catalysts go, factors like economic growth and profitability have paled in comparison to the flow of cheap money stimulus over the last few years. And that flow looks secure for at least another six months. Japan and Europe are succumbing to fresh deflationary pressure, raising expectations of renewed stimulus efforts. The Fed has a market wholly unprepared for higher rates, a job market that hit the skids in September and inflation that has been persistently below its 2 percent target.

After the release of the September meeting minutes, San Francisco Fed President John Williams hit the tape with comments that largely reiterated what he said on Oct. 6: He still expects a rate liftoff this year, still says the September "no hike" policy decision was a close call and still believes there are positive signs coming from the labor market.

Economist Michael Hanson at Bank of America Merrill Lynch believes steady job gains in October and November should keep a December rate hike on track, but does highlight "a significant chance that the FOMC will wait into 2016 before hiking."

These are just teases to maintain the illusion; the history of the last two Fed tightening cycles reveals rate hikes won't happen until the futures market is ready. Current pricing says that won't happen for another six months.

The action in currencies and bonds suggests traders are growing more and more comfortable with the futures market outlook. The dollar is hanging precariously to the bottom of a trading range going back to May. A breakdown in the greenback’s strength based on confirmation that the Fed won’t hike rates this year would set up the first significant pullback since 2013 and put an end to a two-year uptrend — setting off a series of relief rebounds in beaten down assets like crude oil, gold, industrial metals and a variety of related stocks from gold miners to machinery makers like Caterpillar (CAT).

Related: 10 Facts About Janet Yellen, the Most Influential Woman in the World

After dropping from a high in late June, bond market-derived inflation expectations are rising out of a double-bottom pattern traced out since August on expectations of ongoing monetary policy support. High-yield junk bonds are on the move as well, with the iShares High Yield Fund (HYG) up five days in a row, pushing down spreads over Treasury bonds.

Technical indicators also suggest this uptrend is the real deal as the buying has been relentless over the past week. In a note to clients on Thursday, the team at SentimenTrader highlighted two positive developments:

The first is the upward cross of the S&P 500's 50-day moving average, something that hasn't happened since the middle of August. Historically, when this has happened following a correction, buyers have tended to keep pushing stocks up for at least a month.

The second is the triggering of a "Zweig Breadth Thrust," named after Wall Street icon Marty Zweig. This happens when the NYSE 10-day Up Issue indicator goes from below 40 percent to above 61.5 percent within 10 days. This has historically led to consistently positive returns over the medium-term.

Related: Worried About a Recession? Here’s When the Next Slump Will Hit

The last two breadth thrusts were in August 2014 and July 2013, after which stocks rallied 5.8 percent and 11.2 percent, respectively.

Early next year, the rate hike fears will return and this process will start all over again. But for now, it looks like the August-September market spasm was enough to force the Fed to once again give Wall Street what it wants: Another dose of monetary morphine as its zero-interest rate policy looks set to enter its ninth year.