Hey, it’s Friday! Today’s jobs report was very good, but not great — which means it might be just what the economy needs. Here’s what you should know.

Soft Landing Scenario for the Economy Boosted by Latest Jobs Report

Employers added 390,000 new jobs in May and the unemployment rate held steady at 3.6%, the Labor Department announced Friday, boosting hopes that the Federal Reserve can achieve a soft landing as it seeks to control a sustained burst of inflation that threatens to scar the U.S. economy.

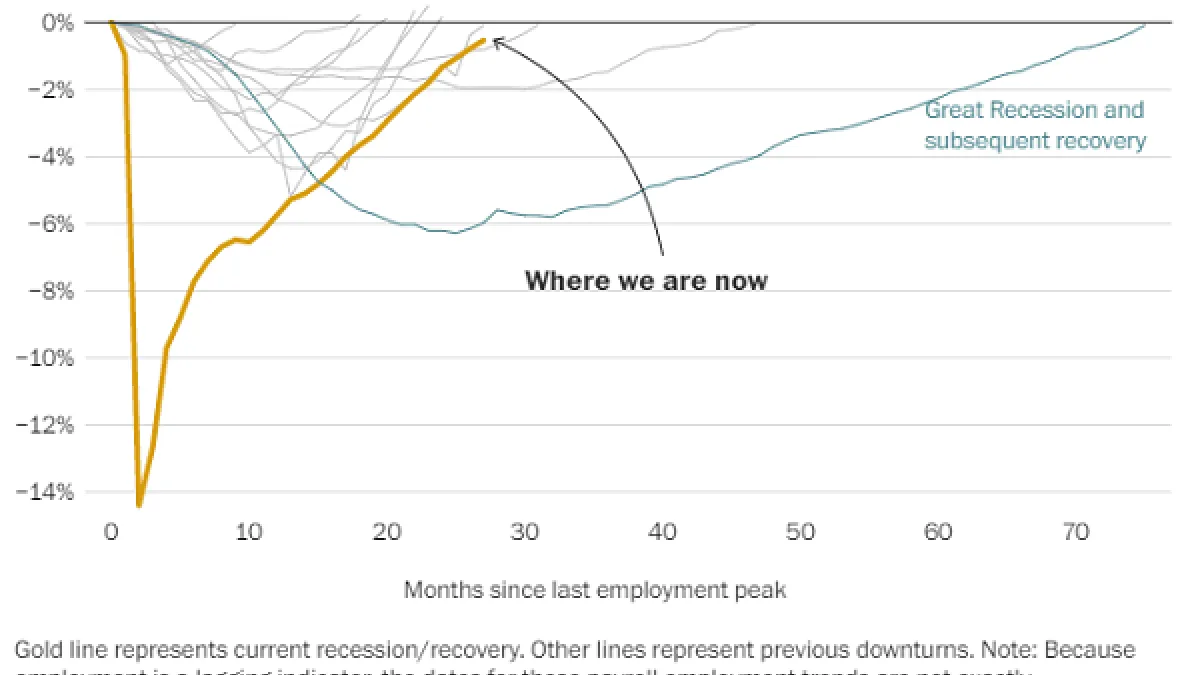

The stronger-than-expected report shows that hiring remains robust, even as the Fed intensifies its effort to tamp down inflation through higher interest rates and quantitative tightening. The labor force participation rate inched a tenth of a point higher, to 62.3%, and with more than 151 million people employed, payrolls are now less than 1 million below the pre-pandemic peak. (The employment chart above from The Washington Post highlights just how strong the recovery has been.)

Although the report beat expectations, the May total did break a 12-month streak of job creation exceeding 400,000 per month. Many analysts see that as good news, suggesting the pandemic recovery is slowing slightly but still far from stall speed. Nominal wage growth also moderated in May, falling from an annual rate of 5.5% to a still-robust 5.2%, helping ease fears about a potential wage-price spiral. Real wage growth, however, was negative, as inflation continued to take a big bite out of worker pay.

“Despite the slight cooldown, the tight labor market is clearly sticking around and is shrugging off fears of a downturn,” economist Daniel Zhao of Glassdoor said in a note. “We continue to see signs of a healthy and competitive job market, with no signs of stepping on the brakes yet.”

Fed still on track: The report offered little support for those hoping the Fed would reconsider its aggressive stance on inflation — a hope that has pushed stocks higher and rates lower over the last week or two.

“We do not expect the Federal Reserve to back off what we expect to be 50 basis-point hikes in the federal funds policy rate in June and July, with the possibility of another in September,” Joseph Brusuelas, chief economist at the consulting firm RSM, said in a note. “In addition, we expect the policy rate to move into restrictive terrain, above 2.5%, before the end of the year, which will create the conditions for further cooling in the labor market that will almost certainly slow down to gains of 200,000 per month in the near term.”

Not surprisingly, interest rates rose Friday, with the 10-year Treasury rate pushing back up close to 3%, and stocks fell as traders considered the increased likelihood of a sustained anti-inflationary campaign by the Fed.

Biden celebrates: President Joe Biden trumpeted the strong report Friday, noting that a record 8.7 million jobs have been created since he took office. And he argued that the economy is now at an inflection point, when inflation will ease and the economy can grow more slowly without tipping into recession.

“We’ve laid an economic foundation that’s historically strong,” he said in Rehoboth Beach, Delaware. “And now we’re moving forward to a new moment, where we can build on that foundation, build a future of stable, steady growth, so we can bring down inflation without sacrificing all the historic gains we’ve made.”

Biden also discussed his plans to combat inflation by lowering the cost of food, fuel and other consumer items, and to reduce the federal budget deficit. (See Biden’s full remarks at CSPAN, with the text available on the White House website.)

What comes next: No one knows, of course, and estimates are all over the map. But the jobs report had some analysts suggesting that the economic trendline is moving toward the Goldilocks scenario: not too hot, not too cold.

RSM’s Brusuelas said he’s confident the economy is slowing, and that the Fed’s anti-inflation campaign is already having its intended effect. “In our estimation, this is likely going to be the last robust employment report in this business cycle,” he wrote. “The delayed impact of past rate hikes is beginning to arrive with an observable slowing of hiring in the rate-sensitive areas of manufacturing, trade and transport, and goods-producing industries, as well as in finance. … Given what was clearly an overheating economy during the final quarter of last year, this jobs report represents a step in the right direction toward restoring price stability, which right now is the paramount policy objective out of Washington.”

Moody’s economist Mark Zandi said the economy is still running too hot but is moving in a healthy direction. “[J]ob growth needs to slow more this summer – get down closer to 150k,” he wrote. “This will ensure the economy doesn’t blow past full-employment, fan wage growth, and exacerbate the high inflation. But today’s job report suggests that’s precisely where the economy is headed.”

But J.P. Morgan Chief U.S. Economist Michael Feroli said that the Fed won’t be satisfied by the slowdown suggested by Friday’s numbers. “It’s moderating, but it’s not moderating to a level, I think, where it’s consistent with the Fed’s inflation goals,” he said of the wage growth data, adding that policymakers would probably want wages to cool toward an annualized 3.5 percent pace, a rate that officials view as aligned with their goal of 2% inflation.

Quote of the Day

“[I] t’s really striking how much doom there is out there from all of these pundits and portfolio managers, who see an imminent recession as a fait accompli, compared with how little evidence there is of that in the data, either from the government or from corporations.”

Bloomberg’s Joe Weisenthal in a newsletter suggesting that the main takeaway from Friday’s jobs data “really is that we’re still not in a recession.”

Despite the positive jobs report, economic warnings from corporate America have been mounting in recent days.

“That hurricane is right out there down the road coming our way,” JPMorgan Chase CEO Jamie Dimon said this week, citing rising interest rates and the war in Ukraine. “We don’t know if it’s a minor one or Superstorm Sandy. You better brace yourself.” Goldman Sachs President John Waldron similarly cautioned that the economy faces extreme challenges. “The confluence of the number of shocks to the system to me is unprecedented,” he said. And Tesla CEO Elon Musk reportedly told employees in emails that he has a "super bad feeling" about the economy and wants to cut about 10% of the nearly 100,000 jobs at the company.

Number of the Day: $1 Billion

Private health insurance companies expect to pay $1 billion in rebates to consumers this fall, according to a preliminary estimate by the Kaiser Family Foundation. The rebates are required under a provision of the Affordable Care Act, which mandated that insurers spend at least 80% of premium payments (85% for large group plans) on medical claims or quality improvement rather than having more money go toward administrative costs or profits. Insurers that fail to meet the threshold must provide rebates to their enrollees. The rebates are calculated based on a three-year average.

This year’s rebate total will be larger than in most prior years, the report says, but will be well shy of the record $2.5 billion issued in 2020, when the Covid-19 pandemic curtailed usual spending on elective and routine care, and the $2 billion issued in 2021. This year’s smaller rebate total comes “in part because 2021 was a less profitable year and because the 3-year window no longer includes 2018, when individual market insurers overpriced their ACA marketplace plans due to uncertainty caused by the repeal-and-replace debate and other ACA policies,” KFF said in a news release.

The new analysis estimates that 8.2 million people are owed a rebate, including 4.3 million people who bought plans on the individual market, which includes the ACA marketplaces. The average rebate per person is projected to be $128. Rebates or rebate notices are due to be sent out by the end of September.

Send your feedback to yrosenberg@thefiscaltimes.com. And please encourage your friends to sign up here for their own copy of this newsletter.

News

- Biden's New Challenge: Putting a Positive Spin on a Slowing Economy – Politico

- Biden’s Challenge: Inflation Overshadows Robust Job Gains – Associated Press

- Senators Make Last-Ditch Bid for Manchin’s Backing – The Hill

- Corporate America Turns Up Volume on Warnings About Economy – Bloomberg

- There’s a Better Solution for Student Loans Than Forgiving Debt, Experts Say – Bloomberg

- America Still Needs More COVID Treatments – Axios

- Watchdog Opens Probe Into Huge Social Security Fines to Poor, Disabled – Washington Post

- Progressives Slam HHS Decision to Keep Higher 2022 Medicare Premium – The Hill

- Biden Keeps Funds Flowing to Build US Electric Vehicle Supply Chain – Bloomberg

- 'Lots of Luck on His Trip to the Moon': Biden Dismisses Musk's Concerns on the Economy – Bloomberg

- More Than Two-Thirds of People Have Covid Antibodies, WHO Says – Bloomberg

- Can Long Covid Lead to Death? A New Analysis Suggests It Could – Politico

Views and Analysis

- The Goldilocks Economy: Trying to Get It ‘Just Right’ – Catherine Rampell, Washington Post

- Fed’s Ideal Jobs Scenario Is Looking More Plausible – Jonathan Levin, Bloomberg

- Latest Jobs Report Shames the Inflation Hawks – Robert Kuttner, American Prospect

- Yellen Wisely Admitted Error on Inflation. The White House Should Follow Her Example – Jennifer Rubin, Washington Post

- The Word Biden Won't Say on Inflation – Felix Salmon, Axios

- Is ‘Greedflation’ Rewriting Economics, or Do Old Rules Still Apply? – Lydia DePillis, New York Times

- Consumers Are Losers in a Booming Industrial Economy – Conor Sen, Bloomberg

- Elon Musk Has a ‘Super Bad Feeling.’ Should Everyone? – Liam Denning, Bloomberg

- What Jamie Dimon Learned From Alan Greenspan – Daniel Moss, Bloomberg

- Now Is No Time to Go Tentative on Military Aid for Ukraine – George F. Will, Washington Post

- Biden Can’t Blame His Staff for His Flailing Presidency – Henry Olsen, Washington Post

- Bribing Some Voters by Forgiving Student Loans May Backfire on Biden – Bernard Goldberg, The Hill

- People, Get Your Booster Shots Already – Faye Flam, Bloomberg

- Doctors Are Still Flying Blind With Paxlovid – Lisa Jarvis, Bloomberg