The average American family has a lot riding on the current debate in Washington over whether “tax expenditures” should be placed on the budget chopping block as part of an effort to reduce the federal deficit.

It has been 25 years since major tax breaks were seriously scrutinized as part of budget negotiations. Back then, under President Ronald Reagan, reductions in tax break for individuals were largely compensated with lower income tax rates. Since then, a thick web of tax deductions, exemptions and credits have crept into the federal tax system, much to the benefit of individuals as well as corporations.

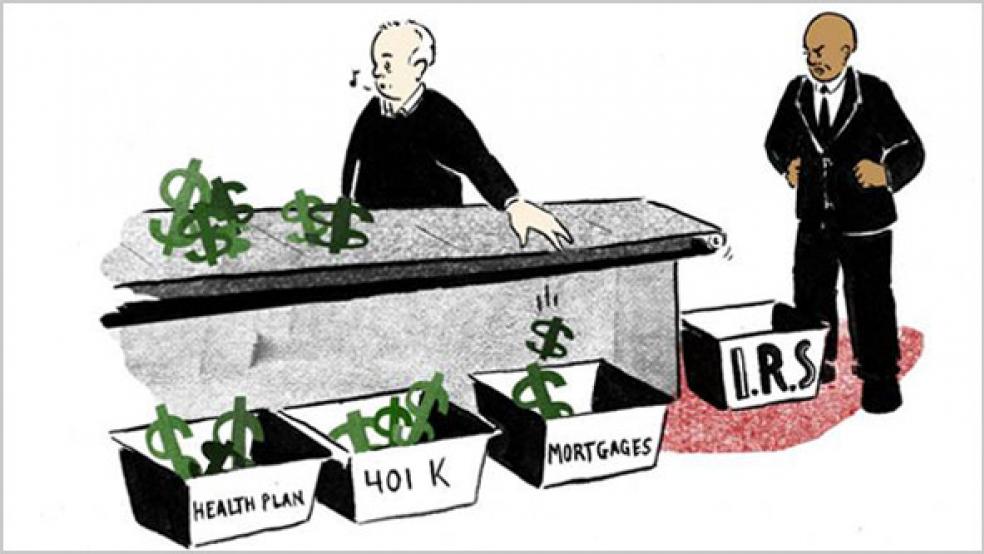

This panoply of tax breaks and subsidies accounts for $1.1 trillion of annual foregone government revenue, and affects virtually every aspect of a family’s life, from buying a home to getting medical treatment sending children to college to retiring in comfort.

An analysis by the accounting firm WeiserMazars shows what a profound economic importance these benefits have to working-class families. If you were to strip away all common tax benefits, an average family of four with a median household income of $61,000 in suburban Maryland would have a federal income tax bill more than six times higher -- $5,954 vs. $774, the analysis shows.

The example is extreme, of course, because no one is seriously suggesting that kind of drastic tax increase on the middle class. But it goes to show how deeply reliant average families are on these subsidies.

Here’s a snapshot of some of the biggest tax subsidies that are sewn so deeply into family finances that they are largely taken for granted:

- Three major homeownership tax breaks add up to $135.7 billion annually in missed revenues for the U.S. government. About $98.5 billion of that is for interest deductions on mortgages of $1million on primary residences and vacation homes.

When selling a home, owners also reap substantial savings from the capital gains exclusion of up to $250,000 for singles – and $500,000 for couples. The perk kept some $27.7 billion out of federal coffers in 2010.

The third-largest homeowner subsidy is the property tax deduction, which has become more valuable in recent years as property taxes have climbed even as home values have declined. This costs the federal government $19.3 billion.

- The largest tax expenditure covers some 60 percent of Americans under age 65 who get insurance through employer-sponsored health plans, the majority of which are paid by their employer. These premiums aren’t included in the gross income of families who benefit from them. This, and the fact that employers get to take a deduction for their contribution, lowers government revenues by $173.7 billion.

The average annual premium for a family’s medical insurance is about $14,700, with the employer typically covering 70%. That’s a tax-free $10,290 for the average family.

- Special tax treatment for retirement savings accounts, a $135.3 billion give-away, includes the ability to shelter income invested in 401(k)s and IRAs from taxes through pre-tax or tax deductible contributions. These accounts increase in value over the long-term on a tax deferred or, in the case of a Roth IRA, tax-free basis.

An estimated 55 million American households participate in 401(k)s or similar defined savings plans, and contribute an average 7 percent of their pre-tax pay, according to The Vanguard Group. In the Weiser analysis, the pre-tax savings in a 401(k) alone cut the average family’s tax bill by 23%. The analysis factored in a contribution of $4,270, which is the average for an income of $61,000, according to Vanguard.

The list goes on – and on. Charitable donation deductions, child tax credits, college credits, special tax treatment for municipal bonds and lower rates on capital gains are among enduring tax breaks.

When it comes to human ecology, however, eliminating or cutting tax breaks may affect more than the spending power of a family or individual.

- Eliminating the mortgage deduction, for example, could cripple sales, or reduce house values even more.

- Add the cost of health insurance to a W-2 filing, and some people will roll the dice and drop out altogether.

- Take away retirement savings benefits and people can't afford to save as much. Then, when they retire, what’s left of Social Security will be their predominant source of income.

- Cut the charitable deduction and people will give less, placing the burden for some social services, among others, squarely back on state and local governments.

Clearly, not all tax breaks are created equal, as anyone who has bounced across tax brackets knows. Many tax benefits notoriously have greater benefits the higher your income. Consider the mortgage interest deduction. “If the government said, ‘The more money you make, the more we’ll give you to pay for it,’ people would say, ‘No way.’ But that’s exactly what happens,” says Roberton Williams, a senior fellow at the Urban Institute. “The value of a deduction is going to be worth a lot more to the rich guy in the 35% tax bracket than for someone in the 10% bracket.”

Many policy analysts say that with the spotlight so squarely on tax expenditures for the first time in generations, it is a prime opportunity to clear out the more wasteful expenditures and to bring more equity to the system. Members of Congress agree with this in theory, but Democrats and Republicans are far from mind-melding when it comes to ways to get this done. While Democrats argue that higher tax revenues should be part of any long term deficit plan, Republicans are adamantly opposed to anything that smacks of a tax increase.

President Obama’s debt reduction plan, unveiled in mid April, aims to equalize the system by capping the value of itemized deductions to 28 percent. This would reduce the benefits of deductions for people in the 33% and 35% income tax brackets. If you are in the 35% tax bracket, the most you would save on a $10,000 deduction would be $2,800, rather than $3,500 without the cap. “That landed with a pronounced thud,” Williams says.

Meanwhile, in House Budget Committee Chairman Paul Ryan’s deficit reduction proposal, supported by many Republicans, he says tax expenditures are a “drag on growth” and he calls for eliminating large ones. Ryan doesn’t give details about which tax expenditures should be eliminated, but he also wants to lower the top individual tax rate from 35 to 25percent, “which would mean eliminating a whole lot of tax expenditures,” says Clint Stretch, director of legislative affairs at Deloitte & Touche.

If Congress starts swinging the axe, the hope is that it does so with surgical precision to prevent the middle class from paying more.

Karen Hube's tax column will also appear this Sunday in the Washington Post Business section.

Related Links:

How Big Are Total Individual Income Tax Expenditures....? (Tax Policy Center)

Deficits: Spending cuts along can't work (CNN)

Boehner: Tie Eliminating Tax Breaks to Lower Corporate Rates (National Journal)