College Students Say They’re Good with Money. Do You Believe Them?

A new study confirms it: College students think they know everything, at least when it comes to personal finance.

Nearly 60 percent of college students said that they had good or excellent financial literacy skills, according to a study released today by the American Institute of CPAs.

Despite that confidence, less than half of students say they stick to a monthly budget, nearly 40 percent had borrowed money from friends or family and more than 10 percent had missed a bill payment.

Of those surveyed, 99 percent said that personal financial management skills were important, but only a quarter said they seek out information on personal finance and incorporate it into their spending and saving habits.

“For many students, college is their first time making financial decisions,” Ernie Almonte, chairman of the AICPA’s Financial Literacy Commission said in a statement. “With this opportunity comes serious responsibility, and if they aren’t making informed, intelligent decisions it can have a negative impact on the rest of their financial lives.”

College students without a strong foundation in personal finance are more likely to take on risky debt or make poor saving decisions. But most students aren’t getting the education they need before they get to campus.

Just 17 states require high school students take a personal finance course, and only six require testing of personal finance concepts, according to the Council for Economic Education. Three out of four American teens can’t even make sense of a paystub.

But hey, at least they’re confident.

Top Reads from The Fiscal Times:

- House GOP Scores a Major Win in Obamacare Legal Challenge

- Hillary’s E-Mail Lapse ... Mistake ... Responsibility ... er, 'Apology'

- How Can You Tell There Are Russian Troops in Syria? Just Look for Some Soldier Selfies

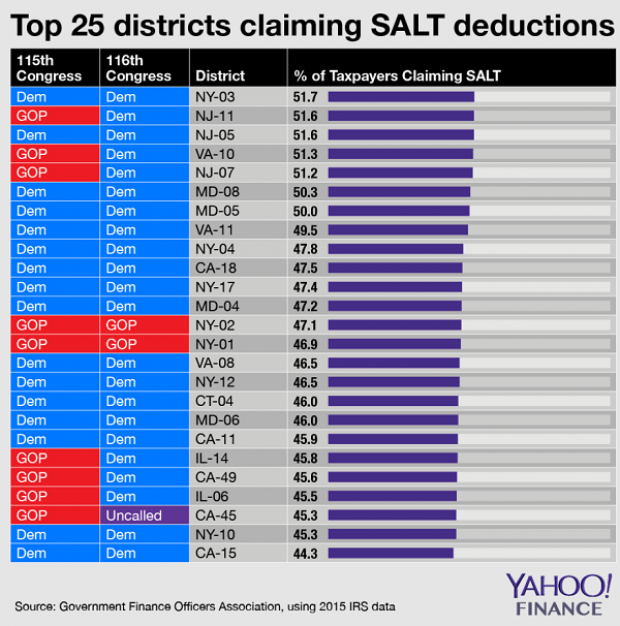

Chart of the Day: SALT in the GOP’s Wounds

The stark and growing divide between urban/suburban and rural districts was one big story in this year’s election results, with Democrats gaining seats in the House as a result of their success in suburban areas. The GOP tax law may have helped drive that trend, Yahoo Finance’s Brian Cheung notes.

The new tax law capped the amount of state and local tax deductions Americans can claim in their federal filings at $10,000. Congressional seats for nine of the top 25 districts where residents claim those SALT deductions were held by Republicans heading into Election Day. Six of the nine flipped to the Democrats in last week’s midterms.

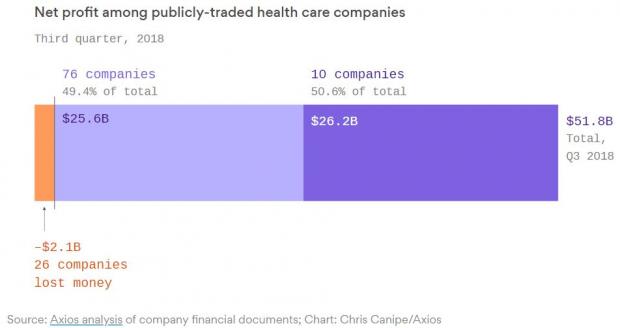

Chart of the Day: Big Pharma's Big Profits

Ten companies, including nine pharmaceutical giants, accounted for half of the health care industry's $50 billion in worldwide profits in the third quarter of 2018, according to an analysis by Axios’s Bob Herman. Drug companies generated 23 percent of the industry’s $636 billion in revenue — and 63 percent of the total profits. “Americans spend a lot more money on hospital and physician care than prescription drugs, but pharmaceutical companies pocket a lot more than other parts of the industry,” Herman writes.

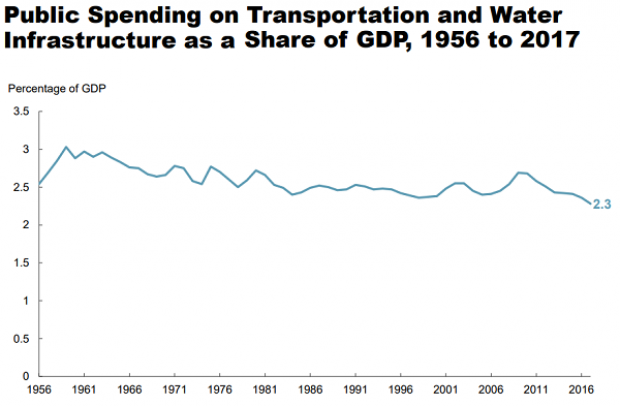

Chart of the Day: Infrastructure Spending Over 60 Years

Federal, state and local governments spent about $441 billion on infrastructure in 2017, with the money going toward highways, mass transit and rail, aviation, water transportation, water resources and water utilities. Measured as a percentage of GDP, total spending is a bit lower than it was 50 years ago. For more details, see this new report from the Congressional Budget Office.

Number of the Day: $3.3 Billion

The GOP tax cuts have provided a significant earnings boost for the big U.S. banks so far this year. Changes in the tax code “saved the nation’s six biggest banks $3.3 billion in the third quarter alone,” according to a Bloomberg report Thursday. The data is drawn from earnings reports from Bank of America, Citigroup, Goldman Sachs, JPMorgan Chase, Morgan Stanley and Wells Fargo.

Clarifying the Drop in Obamacare Premiums

We told you Thursday about the Trump administration’s announcement that average premiums for benchmark Obamacare plans will fall 1.5 percent next year, but analyst Charles Gaba says the story is a bit more complicated. According to Gaba’s calculations, average premiums for all individual health plans will rise next year by 3.1 percent.

The difference between the two figures is produced by two very different datasets. The Trump administration included only the second-lowest-cost Silver plans in 39 states in its analysis, while Gaba examined all individual plans sold in all 50 states.