Love Selfies? Now They Can Keep Your Credit Card Safe

MasterCard is appealing to America’s obsession with selfies in an effort to reduce credit card identity theft.

The credit card company is launching a new program that will allow consumers to approve online purchases with a facial scan. At the checkout page, you’ll be asked to take a picture of yourself using your phone instead of entering a password.

Currently, customers can stop hackers from using their credit card on the Web by setting up a “SecureCode,” which requires a password when shopping online. The password system was used in 3 billion transactions last year.

This fall MasterCard will launch a small pilot program involving 500 customers using fingerprints and facial scans. If the test is a success, the company plans on rolling it out publicly afterward. The company is also looking ahead to one day apply voice recognition technology.

To use the new selfie system, customers need to download the MasterCard phone app. Once you pay for something, a pop-up will appear asking for your authorization with either a fingerprint or facial recognition. Using facial recognition, customers stare at the phone, blink once — and bam! All done. The blink is a security measure so thieves can’t just hold up a photo of you. A fingerprint only requires a touch.

Passwords are easily forgotten, stolen or cracked, so the new system is a way to prove your identity using biometrics. Critics of the new system are uncomfortable that the photo or fingerprint a customer puts into his or her phone will transmit to the company’s computer servers. Cybersecurity experts worry the transfer of such information across devices is too big of a privacy risk.

MasterCard wasn’t the first company to develop a facial recognition app — Chinese shopping brand Alibaba demonstrated one in March, but had to postpone the technology’s launch because of security risks found by China’s central bank and police ministry.

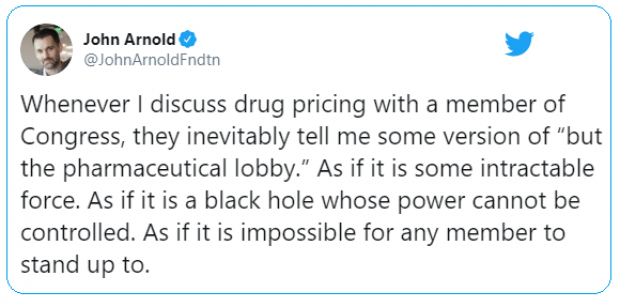

Tweet of the Day: The Black Hole of Big Pharma

Billionaire John D. Arnold, a former energy trader and hedge fund manager turned philanthropist with a focus on health care, says Big Pharma appears to have a powerful hold on members of Congress.

Arnold pointed out that PhRMA, the main pharmaceutical industry lobbying group, had revenues of $459 million in 2018, and that total lobbying on behalf of the sector probably came to about $1 billion last year. “I guess $1 bil each year is an intractable force in our political system,” he concluded.

Warren’s Taxes Could Add Up to More Than 100%

The Wall Street Journal’s Richard Rubin says Elizabeth Warren’s proposed taxes could claim more than 100% of income for some wealthy investors. Here’s an example Rubin discussed Friday:

“Consider a billionaire with a $1,000 investment who earns a 6% return, or $60, received as a capital gain, dividend or interest. If all of Ms. Warren’s taxes are implemented, he could owe 58.2% of that, or $35 in federal tax. Plus, his entire investment would incur a 6% wealth tax, i.e., at least $60. The result: taxes as high as $95 on income of $60 for a combined tax rate of 158%.”

In Rubin’s back-of-the-envelope analysis, an investor worth $2 billion would need to achieve a return of more than 10% in order to see any net gain after taxes. Rubin notes that actual tax bills would likely vary considerably depending on things like location, rates of return, and as-yet-undefined policy details. But tax rates exceeding 100% would not be unusual, especially for billionaires.

Biden Proposes $1.3 Trillion Infrastructure Plan

Joe Biden on Thursday put out a $1.3 trillion infrastructure proposal. The 10-year “Plan to Invest in Middle Class Competitiveness” calls for investments to revitalize the nation’s roads, highways and bridges, speed the adoption of electric vehicles, launch a “second great railroad revolution” and make U.S. airports the best in the world.

“The infrastructure plan Joe Biden released Thursday morning is heavy on high-speed rail, transit, biking and other items that Barack Obama championed during his presidency — along with a complete lack of specifics on how he plans to pay for it all,” Politico’s Tanya Snyder wrote. Biden’s campaign site says that every cent of the $1.3 trillion would be paid for by reversing the 2017 corporate tax cuts, closing tax loopholes, cracking down on tax evasion and ending fossil-fuel subsidies.

Read more about Biden’s plan at Politico.

Number of the Day: 18 Million

There were 18 million military veterans in the United States in 2018, according to the Census Bureau. That figure includes 485,000 World War II vets, 1.3 million who served in the Korean War, 6.4 million from the Vietnam War era, 3.8 million from the first Gulf War and another 3.8 million since 9/11. We join with the rest of the country today in thanking them for their service.

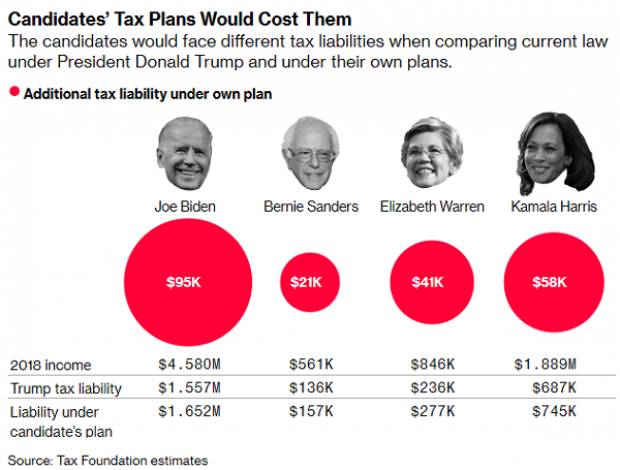

Chart of the Day: Dem Candidates Face Their Own Tax Plans

Democratic presidential candidates are proposing a variety of new taxes to pay for their preferred social programs. Bloomberg’s Laura Davison and Misyrlena Egkolfopoulou took a look at how the top four candidates would fare under their own tax proposals.