Millennials Still Don’t Trust the Stock Market

Goldman Sachs has released the latest in a long line of surveys about millennials and money. The findings won’t shock you if you’ve seen other such surveys: millennials get financial advice from their parents, they’re less concerned with privacy, they still want to own a home … someday.

But one familiar finding may be worth highlighting. Even as the stock market reaches record highs, millennials by and large remain wary of investing. Fewer than 20 percent of those surveyed by Goldman said that stocks are “the best way to save for the future.” Another 45 percent said they’re willing to dip a toe in the market or to put money into low-risk options. More than a third of those surveyed said they don’t know enough about stocks or felt that the market is too volatile or too stacked against small investors.

Part of that may because many millennials haven’t yet reached the life stage or the level of financial stability that would lead them to consider investing. But the lingering scars of the recession are evident in the results, too — and financial institutions clearly have a long way go to restore the public’s confidence in them. For example, Gallup just published a report called, “Why It’s Still Cool to Hate Banks.”

Related: The Rise of a New Economic Underclass—Millennial Men

Goldman didn’t release the details about how many millennials it surveyed or when (and it hadn’t yet responded to an email asking for those details by the time of publication), but the results it got are broadly in line with those of earlier surveys. And they’re another reminder that not everyone is benefitting from the stock market’s record-setting rally. Millennials are still missing out.

Here is a chart produced by Goldman Sachs summarizing the results of their survey:

Deficit Hits $738.6 Billion in First 8 Months of Fiscal Year

The U.S. budget deficit grew to $738.6 billion in the first eight months of the current fiscal year – an increase of $206 billion, or 38.8%, over the deficit recorded during the same period a year earlier. Bloomberg’s Sarah McGregor notes that the big increase occurred despite a jump in tariff revenues, which have nearly doubled to $44.9 billion so far this fiscal year. But that increase, which contributed to an overall increase in revenues of 2.3%, was not enough to make up for the reduced revenues from the Republican tax cuts and a 9.3% increase in government spending.

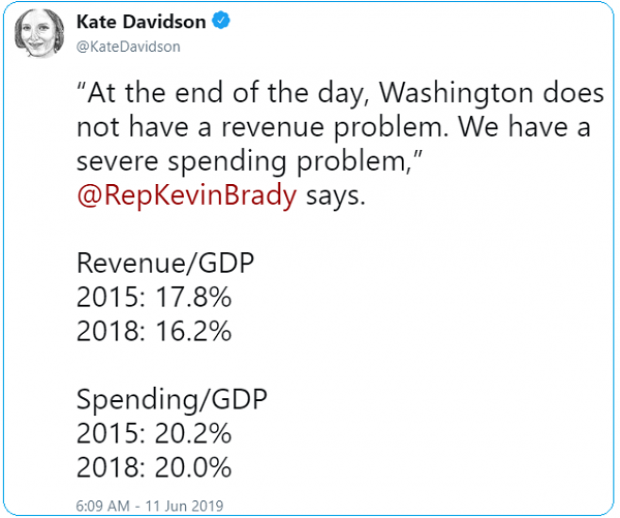

Tweet of the Day: Revenues or Spending?

Rep. Kevin Brady (R-TX), ranking member of the House Ways and Means Committee and one of the authors of the 2017 Republican tax overhaul, told The Washington Post’s Heather Long Tuesday that the budget deficit is driven by excess spending, not a shortfall in revenues in the wake of the tax cuts. The Wall Street Journal’s Kate Davidson provided some inconvenient facts for Brady’s claim in a tweet, pointing out that government revenues as a share of GDP have fallen significantly since 2015, while spending has remained more or less constant.

Chart of the Day: The Decline in IRS Audits

Reviewing the recent annual report on tax statistics from the IRS, Robert Weinberger of the Tax Policy Center says it “tells a story of shrinking staff, fewer audits, and less customer service.” The agency had 22% fewer personnel in 2018 than it did in 2010, and its enforcement budget has fallen by nearly $1 billion, Weinberger writes. One obvious effect of the budget cuts has been a sharp reduction in the number of audits the agency has performed annually, which you can see in the chart below.

Number of the Day: $102 Million

President Trump’s golf playing has cost taxpayers $102 million in extra travel and security expenses, according to an analysis by the left-leaning HuffPost news site.

“The $102 million total to date spent on Trump’s presidential golfing represents 255 times the annual presidential salary he volunteered not to take. It is more than three times the cost of special counsel Robert Mueller’s investigation that Trump continually complains about. It would fund for six years the Special Olympics program that Trump’s proposed budget had originally cut to save money,” HuffPost’s S.V. Date writes.

Date says the White House did not respond to HuffPost’s requests for comment.

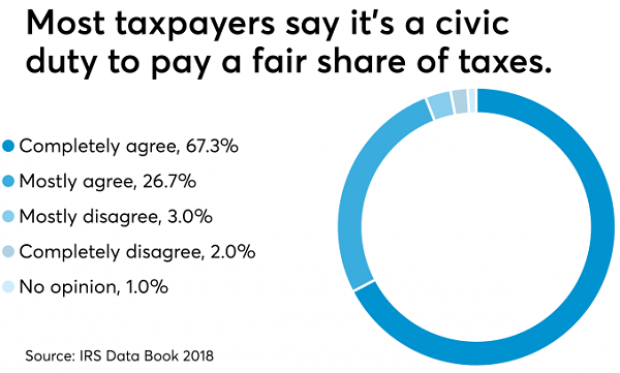

Americans See Tax-Paying as a Duty

The IRS may not be conducting audits like it used to, but according to the agency’s Data Book for 2018, most Americans still believe it’s not acceptable to cheat on your taxes. About 67% of respondents to an IRS opinion survey “completely agree” that it’s a civic duty to pay “a fair share of taxes,” and another 26% “mostly agree,” bringing the total in agreement to over 90%. Accounting Today says that attitude has been pretty consistent over the last decade.