Five States Account for 31% of Underwater Mortgages

Here’s another sign that the housing market keeps getting healthier: More than 250,000 formerly underwater homes regained equity in the first quarter of 2015, according to CoreLogic, meaning that the value of the homes rose above the value of the mortgages on them.

Borrower equity grew more by $694 billion in the quarter, and more than 90 percent of mortgaged American homes now have equity. Such a surge in homeowner wealth has historically led to increased consumer spending and investment.

“Many homeowners are emerging from the negative equity trap, which bodes well for a continued recovery in the housing market,” Anand Nallathambi, president and CEO of CoreLogic said in a statement. “With the economy improving and homeowners building equity, albeit slowly, the potential exists for an increase in housing stock available for sale, which would ease the current imbalance in supply and demand.”

Related: 9 Real Estate Trends to Watch in 2015

Still, 5.1 million mortgaged homes remain underwater, representing 10.2 percent of all mortgaged properties. Five states — Nevada, Florida, Illinois, Arizona and Rhode Island — account for nearly a third of all properties with negative equity. As of the end of the fourth quarter, 10.8 percent of homes — or about 5.4 million properties — were underwater.

The number of underwater homes has decreased year-over-year by 1.2 million and the aggregate value of negative equity has fallen 13 percent to $337.4 billion.

Texas was the state with the fewest underwater properties; 98 percent of homeowners there with a mortgage have equity in their homes.

Just under 20 percent of homes with a mortgage are considered “under-equitied,” meaning that they have less than 20 percent equity and would likely have trouble refinancing their property or obtaining new financing to sell their home and buy another.

A 5 percent increase in home values nationwide would bring another million homeowners into positive equity territory, CoreLogic economists predict.

Quote of the Day: A Big Hurdle for the Tax Cuts

“He goes in and campaigns on an issue, and the challenge is he then talks about executing drug dealers. Why do you think the press is going to cover the tax cuts if you’ve given them the much more exciting issue?”

-- Grover Norquist, president of tax-cutting advocacy group Americans for Tax Reform, on President Trump’s failure to sell the tax law.

The Obamacare Mandate That Could Produce $12 Billion in Fines in 2018

Republicans effectively eliminated the individual Obamacare mandate in the tax package signed late last year. Although the new regulation reducing the mandate penalty to zero doesn’t take effect until 2019, President Trump has cited the rule change as a victory over the health law so many conservatives oppose. “Essentially, we are getting rid of Obamacare. Some people would say, essentially, we have gotten rid of it," Trump told a crowd in Michigan two weeks ago.

However, many parts of the Affordable Care Act are still in effect and will continue to operate even after the individual mandate is eliminated in 2019.

In particular, the employer mandate, which requires companies with more than 50 employees to offer health benefits or face fine of roughly $2,000 per worker, will continue to play a significant role in the Obamacare system. The Congressional Budget Office estimates that the mandate will produce more than $12 billion in fines in 2018 alone.

Some conservative groups are pushing lawmakers to stop enforcing the employer mandate, but the IRS is still working to enforce the law. According to The New York Times Monday, the IRS is sending out notices to more than 30,000 businesses that have failed to comply.

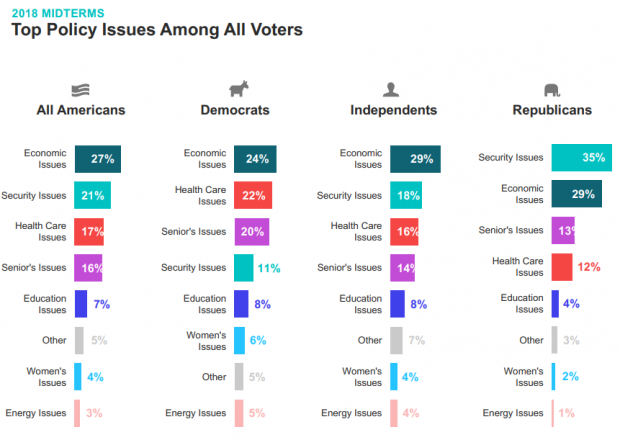

Chart of the Day: It’s Still the Economy, Stupid

Security may be the top policy issue for Republican voters, but the economy is the top concern for Democrats, independents and voters overall, according to Morning Consult’s latest polling on the midterm elections. Health care is third on the list, followed by “seniors’ issues.” The results are based on surveys with more than 275,000 registered U.S. voters from February 1 to April 30.

Number of the Day: $13 Billion

An analysis by Bloomberg finds that the roughly 180 companies in the S&P 500 that have reported earnings for the first three months of the year saved almost $13 billion thanks to the corporate tax cut enacted late last year. Those companies’ effective tax rate dropped by more than 6 percentage points on average. About a third of the tax savings went to 44 financial firms.

How a Florida Doctor with Social Ties to Trump Delayed a $16B Billion VA Project

A West Palm Beach doctor who is friends with Ike Perlmutter, the chairman of Marvel Entertainment and an informal adviser to President Trump on veterans’ issues, has held up “the biggest health information technology project in history — the transformation of the VA’s digital records system,” Politico’s Arthur Allen reports. Dr. Bruce Moskowitz “objected to the $16 billion Department of Veterans Affairs project because he doesn’t like the Cerner Corp. software he uses at two Florida hospitals, according to four former and current senior VA officials. Cerner technology is a cornerstone of the VA project. … Moskowitz’s concerns effectively delayed the agreement for months, the sources said.” Read the full story.