“Federal fiscal policy is entering uncharted territory,” Goldman Sachs economists Alec Phillips and Blake Taylor warned Sunday in a research note. Their title: “What’s Wrong with Fiscal Policy?”

You might know the simple answer: Despite a high national debt and an economy that’s chugging along without much need for additional stimulus, Congress has voted twice in the last two months to significantly expand the budget deficit, first through tax cuts and then through spending increases. But the Goldman Sachs report highlights just how unusual our fiscal policy is at this point — and how little that policy is likely to accomplish over the long term.

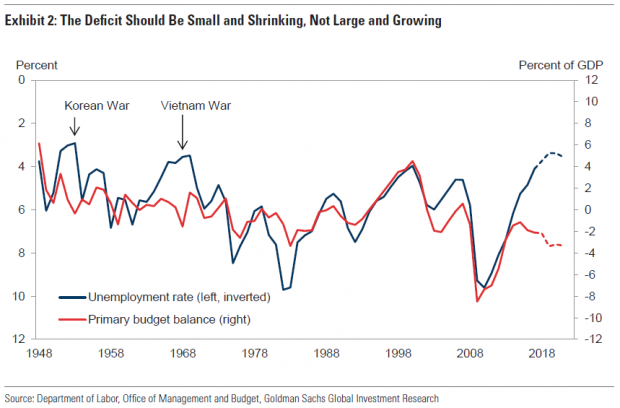

Let’s start with the debt and deficit picture. The level of U.S. debt doesn’t necessarily represent a problem in the short term, Goldman’s economists write, as it falls within the range of several other developed economies — “albeit at the high end of the range.” But the projected deficits lawmakers are racking up at this stage of the economic cycle — and with the debt burden as high as it is — stands out compared to other countries and historical norms.

At this point in the economic cycle, revenues should be rising and spending should be falling. Instead, lawmakers have turned the dials the other way. Government revenues are likely to stay at the low end of their historical range, typically between 15 percent and 20 percent of GDP. And spending looks likely to keep climbing, driven by increases in health care costs on the mandatory side of the federal budget — and the possibility that lawmakers could further boost discretionary spending, too.

“The result,” Goldman’s economists say, “is a cyclically adjusted budget balance [gap] that we project to be wider over the next few years than at any time over the last 50 years with the exception of the 2009- 2012 period following the financial crisis.”

On top of all that, the cost of the federal debt is likely heading much higher as a result of rising interest rates, though it could still be some time before those rising rates push the U.S. debt-to-GDP ratio higher. “As long as the Treasury can borrow at a nominal interest rate below the rate of nominal GDP growth, which we expect will be the case for several more years, the US can run a small primary deficit while maintaining a roughly stable debt-to-GDP ratio,” Goldman’s economists write.

But lawmakers may be setting up a dangerous scenario for U.S. interest costs over the longer term. “We project that, if Congress continues to extend existing policies, including the recently enacted tax and spending legislation, federal debt will slightly exceed 100% of GDP and interest expense will rise to around 3.5% of GDP, putting the US in a worse fiscal position than the experience of the 1940s or 1990s,” the Goldman team writes.

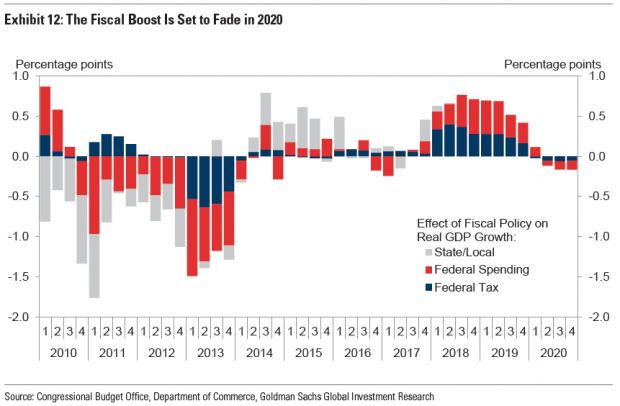

The big question may be what we get for these unusual policies — will the foregone revenues and higher spending pay off in the form of a sustainably stronger economy? The latest analysis, among numerous others, suggests that answer is no. The Goldman economists expect fiscal policy to boost growth by 0.7 percentage points this year and 0.6 percentage points next year — but those growth effects will disappear by 2020. By then, the Goldman economists write, Congress likely won’t be in a position to keep juicing economic growth through even larger deficits.

Still, the economists say that the prospect of meaningful fiscal reforms or shrinking deficits over the next few years remains low. History suggests such changes would require bipartisan efforts, and perhaps a divided government. The path for the next few years appears largely set.